Eric S. Langer, BioPlan Associates06.06.17

The future health and stability of any industry can be difficult to assess. As markets fluctuate, getting a read on where an industry may be headed can be a challenge. Although many metrics are available to evaluate industries, budget analyses can offer a clear assessment of a segment’s strategic direction. When we aggregate individual companies’ strategic funding decisions, we get an overall trend analysis that shows the economically critical business direction that segment is taking.

Budgets and funding can be the canary in the coalmine when it comes to projecting future trends in the biopharmaceutical industry. Examining whether biomanufacturers and contract manufacturing organizations (CMOs) are planning to increase or decrease spending in critical areas gives a good indication of the current health of the industry and the projected growth, or contraction, expected in the future. In BioPlan Associate’s “14th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production,” we surveyed 227 biomanufacturers and CMOs about their budget and planned expenditures. We looked at not only general increases or decreases, but also, over the past eight years, the specific areas those in the industry are planning budget shifts.

Big picture budget issues

Budgets are typically based on pressing strategic needs, and in bioprocessing, when asked what the single most important biomanufacturing trend or operational area on which the industry should focus its efforts, “Manufacturing productivity/efficiency” was the top answer for the fourth year in a row. Biomanufacturers are indicating they want to produce more and do it more efficiently. This clearly factors into budgetary concerns.

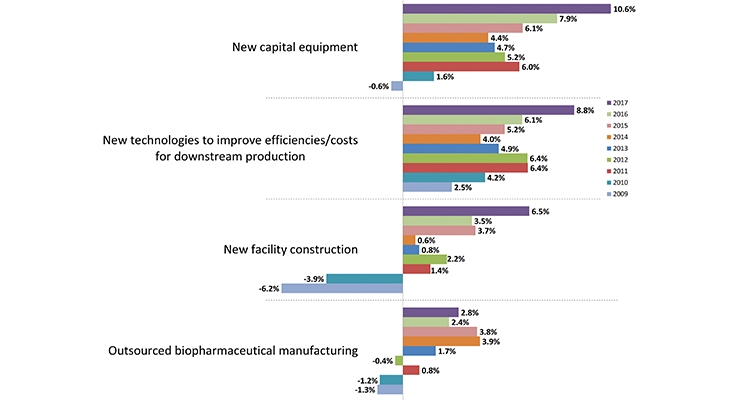

We began measuring budget shifts amidst the drastic economic slowdown beginning in 2008. And current and projected budgets for the biopharmaceutical industry are at some of the highest levels we’ve observed since then. We have asked manufacturers and CMOs their budget trends in 12 key areas since 2009. Over that time, we’ve seen budget swings. But in BioPlan’s 14th Annual Report, we see increases for budgets this year in every area. Not only that, the percent increase reported is the largest ever since 2009 for every category except one (see Figure 1 for selected budget areas).

Increased budgets for new capital equipment

The trend toward the highest increase in budgets in nearly a decade is a clear indication of growth in the industry. The overall picture is important, but examining which areas are seeing the biggest growth is even more informative. From Fig 1, the biggest change was reported in “New capital equipment,” where biopharmaceutical manufacturers and CMOs are reporting an increase of 10.6% for 2017. Budgets for new equipment have been steadily increasing since 2014, indicating the industry’s ability to continue to grow and reinvest in current and future equipment expansions. This is in sharp contrast to the decrease in the budget for new equipment reported in 2009.

Another area related to new capital equipment, signaling long-term growth, is “New facility construction.” Biomanufacturers and CMOs are planning a 6.5% increase in budgets for new facilities. While this is an increase over the last couple of years, this is another area that has seen growth in expenditure the last few years, and has recovered dramatically from a decreased budget in 2009-2010.

The concerns that the industry may have built too much capacity for the pipeline, which surfaced in 2007-2008, resulted in a slowing of new capacity investment while demand and existing supply evened out. The industry is now pivoting towards increasing facility capacity since the fears excess capacity have abated. The increased budgets for new facility construction and new capital equipment are solid indications that the industry is anticipating future growth.

Growth in new technologies for downstream and upstream processing

Another area of anticipated growth, based on projected budgets for this year, is in new technologies. Perhaps this is not much of a surprise as companies are constantly investing in new technologies to grow and change, adapting to innovations like single-use systems and continuous bioprocessing. In this case, biopharmaceutical manufacturers and CMOs reported an 8.8% and 7.7% anticipated increase in 2017 budgets for “New technologies to improve efficiencies/costs for downstream production” and “Upstream production,” respectively. Both of these areas have seen fairly steady budgetary growth in the last 3-4 years. These two categories being the second and third highest expected budgetary growth is not surprising when manufacturing productivity and efficiency is rated the most important trend for the industry.

Downstream processing is often the limiting factor in facility capacity. Chromatography, purification capacity, and filtration tend to be significant budgetary concerns. Large increases in protein expression levels over the past few years have increased pressure on downstream operations and created bottlenecks. Many of the challenges in this arena involve cost. Cost of chromatography materials, cost of membranes, and costs of cleaning and validation are all factors contributing to downstream processing bottlenecks and limiting facility capacity. However, the industry is clearly aware of these budgetary issues, as they have indicated an increase in budget for new technologies for downstream production for the last 4 years, with 2017 being the largest increase ever reported.

Staff hiring and training budgets at all-time high

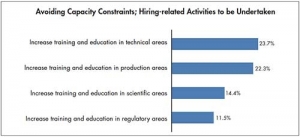

The budgets for staffing are also all being reported at historically high increases. In our survey, we have staffing broken down into 3 different categories. “Training for operations staff” was reported as having the highest increase ever seen at 7.3% for 2017. The hiring budgets for new operations staff and new scientific staff are also expected to have increased budgets this year by 6.9% and 5.7%, respectively. Training is a critical function in bioprocessing, and often correlates to difficulties in hiring operational staff. Productivity increases are typically accompanied by staffing and training budget demands. And future hiring and training can be a bellwether of projections for even further expansions.

Outsourcing budgets

Interestingly, outsourced biopharmaceutical manufacturing is expected to have a relatively small increase in budget this year, only 2.8%. Taken together, this may indicate a flattening or general slow-down of outsourcing, also indicating that biopharmaceutical manufacturers may seek to do their production in-house, rather than increase their overall outsourcing. Even with this relatively low average increase, over 42% of biomanufacturers will be increasing their outsourcing budgets at least somewhat in 2017, up from 36% in 2016.

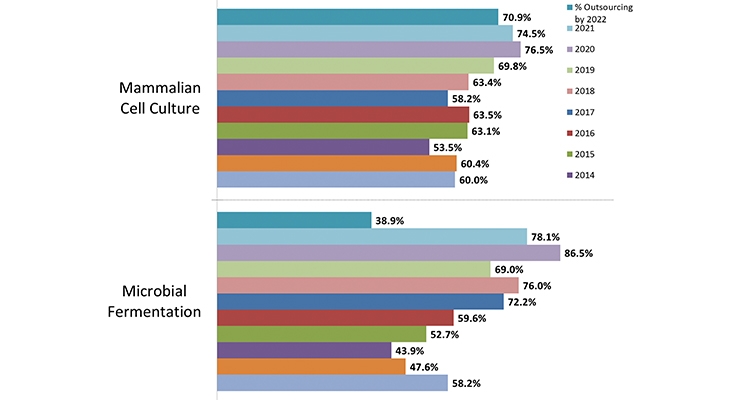

These trends are further confirmed elsewhere in our survey where we asked specifically about outsourcing. We measured the percentage of facilities expecting to outsource substantial production within the next five years (by 2022). We queried regarding mammalian, microbial, yeast, plant and insect systems. In Figure 2, we note that the only type of production expected to generally maintain its outsourcing projections over the next 5 years is mammalian cell culture. In all other areas, manufacturers expect a decrease in outsourcing, including microbial fermentation. It will be interesting to see if the projected outsourcing is an accurate indicator of actual outsourcing over the next 5 years. Historically, mammalian cell culture has been by far the largest segment, and has been increasingly outsourced, but all other areas have been difficult to predict and sometimes shown drastic shifts in expected percentages of outsourcing from year to year.

Budget trends of biopharma suppliers

Biopharmaceutical manufacturers and CMOs are of course the key industry players. However, the opinions of vendors and suppliers for the industry are equally critical in mapping future trends. In BioPlan’s 14th Annual Report, we also asked 131 respondents employed by suppliers about their budgets.

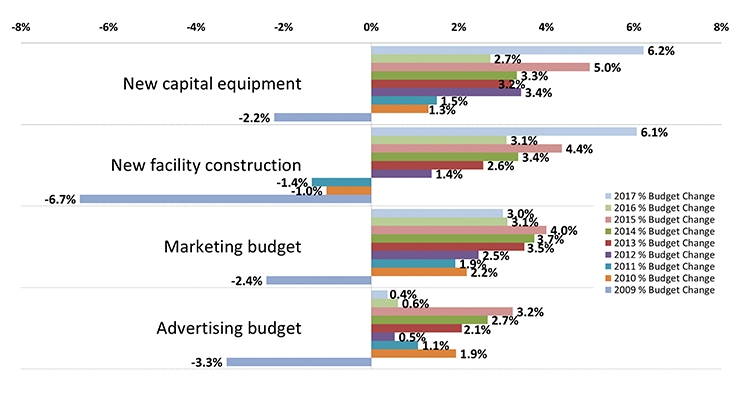

Perhaps unsurprisingly, the budget trends seen for vendors somewhat mirror those seen for manufacturers and CMOs. As seen in Figure 3, vendors are also projecting increased demand, so budgets for “New capital equipment” (6.2%) and “New facility construction” (6.3%) were both reported at historically high levels of anticipated increases over the next year. However, unlike manufacturers and CMOs, those were the only two categories that were reported at such high levels for this year. Most other areas saw either modest growth or a slight decrease in the expected budget for 2017.

Hiring new scientific staff and new commercial staff both saw an increase in budgets for this year over last year, but both of those categories were somewhat lower than the high reported in 2013-2014. And hiring new operations staff actually saw a small decrease in budget for this year compared with 2016.

Based on our analysis, while vendors have clearly recovered from the economic downturn in 2008-2009, they may be operating currently at sufficient capacity to meet the robust growth needs of their biomanufacturing and CMO customers. Separately, we asked vendors to indicate their general sense of optimism about the market. Data indicate a dramatic increase in the percentage of vendors expecting continued ‘above-average’ expectations for financial performance in 2017. With 41% more vendors indicating that they expect to do ‘much better’ this year, compared to last.

While the anticipated budgets are mixed, with 5 of 11 categories reported as an increase for 2017, there are no sharp decreases, and all areas are greatly improved over 2009 budgets.

Will budgets continue to increase?

Biomanufacturers, CMOs, and suppliers, may all have more budget available and are continuing to recover at a healthy pace from the economic downturn. Manufacturers continue to work leaner and harder, trying to do more with less, and we are seeing that the budgetary restrictions are loosening in all areas, particularly those that show far reaching and long-term confidence in the industry, such as new equipment and facility construction.

The focus remains on productivity, which includes cost-cutting measures. Although, it seems that in 2017, companies are looking at efficiency rather than straight cost-cutting since the budgets are expected to increase across the board. As the industry continues to grow and adapt, as it deals with broad factors such as new technologies, companies are continuing to increase budgets by historically high levels in nearly every category. This is an industry whose products are simply needed, and biopharmaceutical products have shown themselves to be largely immune to the worldwide economic problems and recessions.

There is a concern that mergers among large vendors may result in reduced competition, and increased prices. But at present, the new products, innovation, and profitability appear to be relatively in balance, and our study shows, in separate questions, that pricing increases are not ramped up significantly over the past eight years.

The large increases in budgets across the board for manufacturers and CMOs indicate that the biopharmaceutical industry may be headed in a positive direction. Budget increases in long-term investments such as new facilities, equipment, and technologies paint an optimistic picture for the future of the industry.

References

Eric S. Langer

BioPlan Associates

Eric S. Langer is president and managing partner at BioPlan Associates, Inc., a biotechnology and life sciences marketing research and publishing firm established in Rockville, MD in 1989. He is editor of numerous studies, including “Biopharmaceutical Technology in China,” “Advances in Large-scale Biopharmaceutical Manufacturing”, and many other industry reports. elanger@bioplanassociates.com 301-921-5979. www.bioplanassociates.com

Budgets and funding can be the canary in the coalmine when it comes to projecting future trends in the biopharmaceutical industry. Examining whether biomanufacturers and contract manufacturing organizations (CMOs) are planning to increase or decrease spending in critical areas gives a good indication of the current health of the industry and the projected growth, or contraction, expected in the future. In BioPlan Associate’s “14th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production,” we surveyed 227 biomanufacturers and CMOs about their budget and planned expenditures. We looked at not only general increases or decreases, but also, over the past eight years, the specific areas those in the industry are planning budget shifts.

Big picture budget issues

Budgets are typically based on pressing strategic needs, and in bioprocessing, when asked what the single most important biomanufacturing trend or operational area on which the industry should focus its efforts, “Manufacturing productivity/efficiency” was the top answer for the fourth year in a row. Biomanufacturers are indicating they want to produce more and do it more efficiently. This clearly factors into budgetary concerns.

We began measuring budget shifts amidst the drastic economic slowdown beginning in 2008. And current and projected budgets for the biopharmaceutical industry are at some of the highest levels we’ve observed since then. We have asked manufacturers and CMOs their budget trends in 12 key areas since 2009. Over that time, we’ve seen budget swings. But in BioPlan’s 14th Annual Report, we see increases for budgets this year in every area. Not only that, the percent increase reported is the largest ever since 2009 for every category except one (see Figure 1 for selected budget areas).

Increased budgets for new capital equipment

The trend toward the highest increase in budgets in nearly a decade is a clear indication of growth in the industry. The overall picture is important, but examining which areas are seeing the biggest growth is even more informative. From Fig 1, the biggest change was reported in “New capital equipment,” where biopharmaceutical manufacturers and CMOs are reporting an increase of 10.6% for 2017. Budgets for new equipment have been steadily increasing since 2014, indicating the industry’s ability to continue to grow and reinvest in current and future equipment expansions. This is in sharp contrast to the decrease in the budget for new equipment reported in 2009.

Another area related to new capital equipment, signaling long-term growth, is “New facility construction.” Biomanufacturers and CMOs are planning a 6.5% increase in budgets for new facilities. While this is an increase over the last couple of years, this is another area that has seen growth in expenditure the last few years, and has recovered dramatically from a decreased budget in 2009-2010.

The concerns that the industry may have built too much capacity for the pipeline, which surfaced in 2007-2008, resulted in a slowing of new capacity investment while demand and existing supply evened out. The industry is now pivoting towards increasing facility capacity since the fears excess capacity have abated. The increased budgets for new facility construction and new capital equipment are solid indications that the industry is anticipating future growth.

Growth in new technologies for downstream and upstream processing

Another area of anticipated growth, based on projected budgets for this year, is in new technologies. Perhaps this is not much of a surprise as companies are constantly investing in new technologies to grow and change, adapting to innovations like single-use systems and continuous bioprocessing. In this case, biopharmaceutical manufacturers and CMOs reported an 8.8% and 7.7% anticipated increase in 2017 budgets for “New technologies to improve efficiencies/costs for downstream production” and “Upstream production,” respectively. Both of these areas have seen fairly steady budgetary growth in the last 3-4 years. These two categories being the second and third highest expected budgetary growth is not surprising when manufacturing productivity and efficiency is rated the most important trend for the industry.

Downstream processing is often the limiting factor in facility capacity. Chromatography, purification capacity, and filtration tend to be significant budgetary concerns. Large increases in protein expression levels over the past few years have increased pressure on downstream operations and created bottlenecks. Many of the challenges in this arena involve cost. Cost of chromatography materials, cost of membranes, and costs of cleaning and validation are all factors contributing to downstream processing bottlenecks and limiting facility capacity. However, the industry is clearly aware of these budgetary issues, as they have indicated an increase in budget for new technologies for downstream production for the last 4 years, with 2017 being the largest increase ever reported.

Staff hiring and training budgets at all-time high

The budgets for staffing are also all being reported at historically high increases. In our survey, we have staffing broken down into 3 different categories. “Training for operations staff” was reported as having the highest increase ever seen at 7.3% for 2017. The hiring budgets for new operations staff and new scientific staff are also expected to have increased budgets this year by 6.9% and 5.7%, respectively. Training is a critical function in bioprocessing, and often correlates to difficulties in hiring operational staff. Productivity increases are typically accompanied by staffing and training budget demands. And future hiring and training can be a bellwether of projections for even further expansions.

Outsourcing budgets

Interestingly, outsourced biopharmaceutical manufacturing is expected to have a relatively small increase in budget this year, only 2.8%. Taken together, this may indicate a flattening or general slow-down of outsourcing, also indicating that biopharmaceutical manufacturers may seek to do their production in-house, rather than increase their overall outsourcing. Even with this relatively low average increase, over 42% of biomanufacturers will be increasing their outsourcing budgets at least somewhat in 2017, up from 36% in 2016.

These trends are further confirmed elsewhere in our survey where we asked specifically about outsourcing. We measured the percentage of facilities expecting to outsource substantial production within the next five years (by 2022). We queried regarding mammalian, microbial, yeast, plant and insect systems. In Figure 2, we note that the only type of production expected to generally maintain its outsourcing projections over the next 5 years is mammalian cell culture. In all other areas, manufacturers expect a decrease in outsourcing, including microbial fermentation. It will be interesting to see if the projected outsourcing is an accurate indicator of actual outsourcing over the next 5 years. Historically, mammalian cell culture has been by far the largest segment, and has been increasingly outsourced, but all other areas have been difficult to predict and sometimes shown drastic shifts in expected percentages of outsourcing from year to year.

Budget trends of biopharma suppliers

Biopharmaceutical manufacturers and CMOs are of course the key industry players. However, the opinions of vendors and suppliers for the industry are equally critical in mapping future trends. In BioPlan’s 14th Annual Report, we also asked 131 respondents employed by suppliers about their budgets.

Perhaps unsurprisingly, the budget trends seen for vendors somewhat mirror those seen for manufacturers and CMOs. As seen in Figure 3, vendors are also projecting increased demand, so budgets for “New capital equipment” (6.2%) and “New facility construction” (6.3%) were both reported at historically high levels of anticipated increases over the next year. However, unlike manufacturers and CMOs, those were the only two categories that were reported at such high levels for this year. Most other areas saw either modest growth or a slight decrease in the expected budget for 2017.

Hiring new scientific staff and new commercial staff both saw an increase in budgets for this year over last year, but both of those categories were somewhat lower than the high reported in 2013-2014. And hiring new operations staff actually saw a small decrease in budget for this year compared with 2016.

Based on our analysis, while vendors have clearly recovered from the economic downturn in 2008-2009, they may be operating currently at sufficient capacity to meet the robust growth needs of their biomanufacturing and CMO customers. Separately, we asked vendors to indicate their general sense of optimism about the market. Data indicate a dramatic increase in the percentage of vendors expecting continued ‘above-average’ expectations for financial performance in 2017. With 41% more vendors indicating that they expect to do ‘much better’ this year, compared to last.

While the anticipated budgets are mixed, with 5 of 11 categories reported as an increase for 2017, there are no sharp decreases, and all areas are greatly improved over 2009 budgets.

Will budgets continue to increase?

Biomanufacturers, CMOs, and suppliers, may all have more budget available and are continuing to recover at a healthy pace from the economic downturn. Manufacturers continue to work leaner and harder, trying to do more with less, and we are seeing that the budgetary restrictions are loosening in all areas, particularly those that show far reaching and long-term confidence in the industry, such as new equipment and facility construction.

The focus remains on productivity, which includes cost-cutting measures. Although, it seems that in 2017, companies are looking at efficiency rather than straight cost-cutting since the budgets are expected to increase across the board. As the industry continues to grow and adapt, as it deals with broad factors such as new technologies, companies are continuing to increase budgets by historically high levels in nearly every category. This is an industry whose products are simply needed, and biopharmaceutical products have shown themselves to be largely immune to the worldwide economic problems and recessions.

There is a concern that mergers among large vendors may result in reduced competition, and increased prices. But at present, the new products, innovation, and profitability appear to be relatively in balance, and our study shows, in separate questions, that pricing increases are not ramped up significantly over the past eight years.

The large increases in budgets across the board for manufacturers and CMOs indicate that the biopharmaceutical industry may be headed in a positive direction. Budget increases in long-term investments such as new facilities, equipment, and technologies paint an optimistic picture for the future of the industry.

References

- 14th Annual Report and Survey of Biopharmaceutical Manufacturing Capacity and Production, April 2017, BioPlan Associates, Inc. www.bioplanassociates.com

Eric S. Langer

BioPlan Associates

Eric S. Langer is president and managing partner at BioPlan Associates, Inc., a biotechnology and life sciences marketing research and publishing firm established in Rockville, MD in 1989. He is editor of numerous studies, including “Biopharmaceutical Technology in China,” “Advances in Large-scale Biopharmaceutical Manufacturing”, and many other industry reports. elanger@bioplanassociates.com 301-921-5979. www.bioplanassociates.com